Conditions for obtaining a military mortgage

Participants in the program from Rosvoenipoteka can include people who have entered into a contract and work in the structures of the Russian Ministry of Defense, the National Guard, the Federal Security Service, the FSB, the Ministry of Emergency Situations, military personnel of the Special Objects Service under the President of the Russian Federation and the Prosecutor General's Office.

Everyone who entered at least three years of service from December 31, 2019, including previously existing contracts, is automatically included in the savings-mortgage system.

Important: you can take advantage of the benefit within 10 years from the date of entry into service or study.

What kind of housing can you buy?

Using military mortgage funds, you can buy an apartment or a room in a finished house, a residential building with a plot of land, a town house and an apartment in a new building. The program does not limit the purchase of real estate in any region of the country. Moreover, some banks allow you to use money to repay a previously issued home loan.

But it is worth emphasizing that the issue of purchasing apartments using military mortgages in new buildings sold through escrow accounts has not yet been legally regulated.

How much funding will be allocated in 2021?

The maximum amount of a home loan for military personnel usually does not exceed 2.9 million rubles, depending on the bank regulations.

In this case, it is allowed to purchase an apartment at a price above the limit, but subject to the approval of this transaction by a credit institution. In this case, the employee will have to pay the difference himself.

Military mortgage funds can be combined with housing certificates and social payments such as maternity capital.

How to get a military mortgage to buy an apartment in a new building in 2021?

Initially, the serviceman must write a report addressed to the unit commander to obtain a certificate of a targeted housing loan (validity period of the Central Housing Loan - 6 months), then submit it to the bank along with an identity card to obtain preliminary approval for a mortgage. The financial institution will also provide a list of accredited developers and/or new buildings, if there are any restrictions.

After choosing an apartment, you must provide the credit institution with a standard mortgage package of documents:

- passport and military ID,

- certificate of targeted housing loan,

— notarized consent of the spouse to complete the transaction or marriage contract,

- birth certificates of children,

— a preliminary agreement on the conclusion in the future of an agreement for participation in shared construction of a residential building,

— additional documents at the bank’s request.

An account is opened at the bank to receive funds.

Expert opinion

Kozlov Andrey Kirillovich

Lawyer with 10 years of experience. Specialization: criminal law. More than 3 years of experience in developing legal documentation.

The next step will be the conclusion of an agreement on the central housing estate with the Federal State Institution "Rosvoenipoteka", the signing of a loan agreement with the bank and an equity participation agreement (DPA) with the seller of the apartment in the new building. All documents related to the transaction are sent to Rosvoenipoteka.

Conditions for approving a military mortgage in 2021

Mortgages for military personnel are provided for a period of up to 20 years, while the age of the borrower at the time of the last payment should not exceed 45 years.

The purchased home will be used as collateral, just like with a regular home loan. Registration of necessary insurance policies is mandatory.

The savings and mortgage system should become the main tool for providing military personnel with housing in the coming years

According to the Russian Ministry of Defense, the popularity of military mortgages has increased by more than 2.5 times since 2012. Today, the number of participants in this system exceeds the total number of those who received permanent housing or housing certificates and subsidies from the department.

Providing housing for different categories of the population and, in particular, military personnel is still one of the most pressing problems of Russian society. Until December 2021, apartments for military personnel were distributed by the Housing Department of the Russian Ministry of Defense.

But 01.01. 2021 a new law came into force: obtaining housing on a first-come, first-served basis was replaced by a mortgage for military personnel under a contract.

Its conditions in 2021 apply to certain categories of defenders of the Motherland. Let's look at them and find out who can count on a military mortgage.

- How does a mortgage work for contract workers?

- Special conditions

- Who is it for?

- About the advantages and disadvantages

- Conditions for contract military personnel

- How to get a mortgage

- Participating banks

- Changes in military mortgage: Video

How does a mortgage work for contract workers?

There has been a military mortgage with government support for more than 10 years. At the same time, all military personnel are provided with an individual approach when creating a loan plan.

A mortgage for military contractors is similar to a mortgage agreement with a bank, however, the first amount is transferred to the borrower’s account from the state budget, and further monthly payments are made by the Ministry of Defense.

The main condition for participation in this program is the funded mortgage system (the abbreviation NIS is often used).

After joining the NIS, funds transferred by the state for the purchase of housing begin to accumulate on the serviceman’s personal account. They are transferred throughout their entire service life - twenty years.

However, there is a limitation on the period of their use: a military mortgage for military personnel under a contract allows you to purchase a home after at least three years of service.

Special conditions

A situation may arise when the funds available in the account have not been spent. In this case, the serviceman has the right to use them for any purpose. However, like any program, this state system has some conditions that should be taken into account before using the accumulated finances.

Briefly, these conditions are formulated as follows:

- As the service life increases, the amount of subsidies increases.

- Families with three or more children receive an advantage in obtaining a military mortgage.

- You can use government assistance to purchase housing only once.

Who is it for?

Mortgages for military personnel under a contract apply to military personnel of the following categories:

- Warrant officers, officers who entered into long-term contracts after January 1, 2005.

- Graduates of military universities who serve on long-term contracts starting in 2005 and in later years.

- Military personnel in the position of midshipman or warrant officer who have served three or more years. First contract.

- Sailors, soldiers, sergeants, foremen who took office in 2005 and later. Re-contract.

Not only those who are serving, but also military personnel who were forced to leave the army for the following reasons can receive a military mortgage loan:

- dismissal for health reasons;

- dismissal for family reasons;

- resignation due to staffing and organizational changes;

- reaching the age limit.

There is also a special condition for military personnel who entered into a contract before 2005. They have the right to participate in the mortgage lending program, but without opening a savings account.

Military mortgage for those discharged at a certain age

The age limit for military personnel is 50 years. Upon dismissal due to age, accumulations in the personal account cease. Accordingly, the remaining amount of the loan will have to be paid independently. The earlier a military mortgage is issued, the greater the likelihood of full repayment using mortgage savings.

This is important to know: How to get a company apartment for employees

Repayment of a military mortgage upon dismissal after 35 years is made by the state in the case of service of more than 10 years in the presence of preferential circumstances, or 20 years without them. In other cases, it is necessary to compensate the state for the funds spent, including the savings in the personal account used for the down payment.

About the advantages and disadvantages

A mortgage for NIS participants has the following advantages:

- You can find housing in any region of Russia.

- Fixed interest rate. Its value is not affected by either the repayment period or the amount of the down payment.

- Not only senior officers, but also young military personnel whose age does not exceed 25 years can purchase housing.

- Military mortgages for contract soldiers allow the use of maternity capital.

- Guarantee of government payments. The participant’s personal account will be replenished even if the loan is repaid early.

- Military personnel who previously inherited residential real estate, received it as a gift, or purchased it are eligible for a subsidy.

The only drawback (it would be more appropriate to use the word “risk” here) can be considered dismissal from the armed forces. If this happened due to circumstances discrediting the serviceman, he is obliged to repay the amounts spent on repaying the loan by the authorized federal body within a ten-year period.

The same applies to military personnel with less than 10 years of service who were dismissed due to regular circumstances. Payments must be made monthly, interest is charged only on the outstanding balance.

Conditions for contract military personnel

This issue was partially touched upon above. Let's add only the main points.

Expert opinion

Kozlov Andrey Kirillovich

Lawyer with 10 years of experience. Specialization: criminal law. More than 3 years of experience in developing legal documentation.

Firstly, you should know that when issuing such a loan, the composition of the family does not affect the amount of the amount. Even if a serviceman has five rather than one child, the size of the bank loan will be standard.

In this case, the living space is registered in the name of the serviceman. It’s a different matter when maternity capital is used to repay the loan: then housing is divided equally between family members.

Secondly, if the spouses are officers, both of them can legally become participants in the NIS. But you won’t be able to get one apartment for two targeted housing loans.

Thirdly, using a military mortgage to build a house is not provided for by its original conditions. But this can be done by retiring from the armed forces upon reaching the age limit. After all, you can spend the funds remaining in your savings account at your own discretion.

The volume of lending is a very important factor. The class of housing that will allow contract servicemen to purchase a mortgage depends on it. The terms of the program from this point of view are as follows:

- The maximum loan amount is no more than 2.4 million rubles. Until 2021, this figure was lower - 2.4 million.

- The borrower must have his own funds, adding which to those accumulated under the NIS program, he will be able to make a down payment in the amount of 20% of the appraised value of the housing. This is a very important point for those who want to know how to get a military mortgage for a contractor under 2021 conditions.

- The interest rate cannot exceed 12.5% per annum. Typically this figure ranges from 8-12%.

How to get a mortgage

To do this, you must complete the following steps:

- Draw up a report addressed to your unit commander about your desire to become a participant in the state military mortgage lending program.

It is important to know: officers are not required to do this, since information about them is already in the register.

- After this, the High Command of the Armed Forces checks all participants using the available lists and, based on the identified need, creates a list of documents that is transferred to the housing department.

- The military man who submitted the report is assigned a personal registration number. He receives it in a notification.

- Next, on the basis of the NIS, the state support program “Rosvoenipoteka” opens an account for the serviceman.

- Receipts to this account will begin immediately after the report is registered in the unit.

- The service member then selects a bank to receive funds.

- After this, the serviceman chooses housing. A military mortgage allows you to purchase an apartment on both the primary and secondary markets.

- An agreement is concluded with the bank.

- A serviceman purchases housing through a mortgage program.

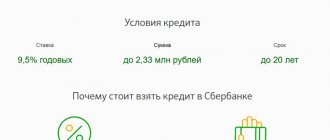

Participating banks

Having learned how a contractor can get a military mortgage, you can begin choosing a lending institution. The data in the table below will allow you to navigate the financial market segment under consideration.

| Bank | Program | Loan amount, rub. | Bid, % | Term |

| Sberbank | Military mortgage | 2.33 million | 9,5 | Up to 20 years |

| Gazprombank | Military mortgage | 2.33 million | 9,5 | Up to 20 years |

| Svyaz-bank | Military mortgage | 400 thousand - 2.1 million | Basic 10.9 | 3-20 years |

| VTB 24 | Mortgage for the military | 2.29 million | from 9.7 to 10 | Up to 20 years |

To summarize, it must be said that the government’s cooperation with financial organizations in the system of preferential lending to military personnel is an effective measure to resolve the problems of Russian citizens with the purchase of personal housing.

Dismissal with military service from 10 to 20 years due to general injury

Operational and staffing measures (OSM) are carried out in the ranks of the Armed Forces in order to reorganize personnel and can provoke the termination of a military contract in the following cases:

- when changing staff;

- when reducing positions;

- if the employee is not suitable for the position held;

- upon expiration of the military contract.

Participants in the military mortgage program who have served from 10 to 20 years, using preferential terms of dismissal under the general military service, can count on the gratuitous nature of housing and monthly payments, as well as the removal of state encumbrance from the apartment. Additional accruals are due to those military personnel whose military service at the time of leaving the Armed Forces has not reached 20 calendar years.

Description of military mortgage

Military mortgage is a government program that began to be implemented in practice in 2005 and has become the main mechanism for citizens undergoing military service to purchase their own housing. Its economic, legal and social foundations are regulated by a law adopted in August 2004, which has federal significance and is called “On the savings and mortgage system of housing for military personnel.”

The bottom line is that first, a military man applying for the purchase of residential property on special terms becomes involved in the so-called savings-mortgage system (common abbreviation - NIS). He enters into this program automatically if he has concluded his first contract since the beginning of 2005.

In other cases, a citizen must declare his desire to join the NIS.

Every year, the state transfers savings contributions from the federal budget to the individual account of a military serviceman, forming capital intended for housing. After a three-year period of service, a military man can exercise the right to acquire real estate.

The accumulated funds are used as a mandatory down payment. Next, monthly payments are transferred to the bank by the federal state government institution (FGKU) Rosvoenipoteka, established under the Russian Ministry of Defense.

Funds allocated from the federal budget have a strictly designated purpose, that is, during the period of service they can be used exclusively to provide the serviceman with his own housing. If a military man ceases to be a member of the NIS, that is, leaves service at his own request or for other reasons, then he continues to make regular payments from his own budget.

Moreover, if the reasons for dismissal are not valid, then the serviceman also undertakes to return all money previously spent. This leads to huge debts.

For your information! If during the period of his service a serviceman has not exercised his legal right to purchase housing, then upon dismissal for good reasons (they will be discussed below), he can receive the accumulated funds and spend them at his discretion on any needs other than housing.

How is a military mortgage paid to a bank?

Having become a member of the NIS, a serviceman receives a personal account. The account is replenished with annual contributions from the federal budget. It is these payments that are transferred to the bank to pay off the loan and are used for the down payment.

The real estate registered under the purchase and sale agreement remains pledged to the credit institution until the mortgage obligations are fully fulfilled. The actual payer of the mortgage loan is the Ministry of Defense. During the loan repayment period, the serviceman’s personal account is not replenished, since all funds are transferred directly to the bank.

Important! Applying for a mortgage is accompanied by additional expenses: home appraisal, life insurance of the borrower and collateral real estate. These expenses are paid by the program participant from his own budget.

Current situation

The conditions for providing a mortgage for this current year 2021 are as follows:

- The funds transferred to the borrower's savings account by the state are used after 3 years of service to form the entry fee. And to pay for the remaining part of the price of the purchased residential property, the lending bank provides a mortgage, which is repaid by state-directed contributions within the NIS (while the client participates in the system, that is, continues to serve).

- The final total amount of the mortgage loan at the moment is a maximum of 2 million and 570 thousand Russian rubles.

- The down payment amount is at least 15%.

- The interest rate is 9.2% per annum. Moreover, this indicator remains the same even if the payer leaves NIS and makes regular payments independently at the expense of his own finances.

- Mortgage payment terms range from a minimum of thirty-six months (that is, three years) to a maximum of twenty years. But the permissible length of the period depends on the age of the borrower: he can repay the mortgage on NIS terms up to a maximum of his 45 years (inclusive). This means that if the applicant is 35 years old at the time of applying for a housing loan, then he will be able to obtain a mortgage for a maximum of ten years.

- A potential client of a financial organization may not have to confirm his solvency, because if he is a military serviceman and a member of the NIS, then the state will regularly make payments for him.

For your information! These conditions are principles that apply to all Russian financial organizations implementing military mortgage lending programs. That is, the bank cannot independently revise the rules, since they are established by the legislation in force in the country.

Early repayment

If the appropriate opportunity arises, a serviceman has the right to repay the mortgage issued to him ahead of schedule, for example, from his own savings or with the help of maternity capital issued at the birth of a second or subsequent child. But the borrower must notify, firstly, the Federal State Institution “Rosvoenipoteka” of such intentions, and secondly, the lending bank (not all financial organizations allow the closure of the contract ahead of schedule).

If, after early repayment, there are savings left in the military account, he can receive them and use them at his own discretion for any purpose, subject to the following conditions:

- length of service exceeds 20 years;

- 10 years of service and dismissal for reasons such as injuries or illnesses acquired in the service, forced staff reductions, or difficult family circumstances (for example, the need for constant care for a seriously ill relative).

In such situations, you must first notify the bank that issued the housing loan about unscheduled or increased payments. Write an application for early repayment and receive a new payment schedule.

Next, contact Rosvoenipoteka and file an appeal there. Please attach a loan statement, certificates of additional payments and an updated schedule to your application.

Also, the possibility of early repayment of an issued military mortgage appears if the savings contributions exceed the monthly payments transferred to the bank. In this case, there are funds left in the account that can be used to make additional unscheduled payments.

To make an early unscheduled payment, you must first find out the size of the balance, then contact the institution “Rosvoenipoteka” with treatment according to the standard. Within thirty days, the Federal State Budgetary Institution makes a decision, after which the payer contacts the bank with an application for early repayment and a request for a new schedule.

Misuse of funds

If during the entire period of service a citizen has not decided to take advantage of the legal right and acquire personal housing with state support, then he can still receive the accumulated funds and spend them on any other needs, for example, on purchasing a personal car or opening a deposit.

If a serviceman goes into the reserve, he can count on receiving the savings generated within the NIS only if his service is at least twenty years. If you have served for at least 10 years, you can receive such funds only in case of dismissal for good reasons: due to deteriorating health (injury received during service or acquired illness), changed family circumstances (for example, forced constant care for a disabled relative) or due to a reduction in military personnel.

Coming Changes

The latest news says that some adjustments will be made to the savings-mortgage system. They will affect the list of NIS participants, as well as the amounts allocated from the state. budget funds.

Participants

Starting from 2021, the list of participants in the existing savings mortgage system in Russia will expand. At the moment, only representatives of the officer corps can become them.

Starting next year, the list will include sergeants, sailors, foremen and ordinary soldiers. But such military personnel must come to service after the end (December thirty-first) of the current year 2019, that is, from the first of January of the coming 2021.

At the same time, their total duration of contract service after the end of 2019 must be at least 3 years to exercise the right to secure real estate under a mortgage (the period of service before the specified date will also be taken into account).

Until the changes in legislation came into force, only officers, midshipmen and warrant officers with a total duration of contract service of three years (starting from two thousand and five) or those who began contract service had the opportunity to participate in the program. as well as re-serving sailors, sergeants, petty officers and soldiers.

Good to know! The adjustments are due to changes that were made to the eighth and ninth articles of federal law number 117, adopted in 2004.

With the onset of 2021, the military mortgage program, implemented with state support, will become the only form of providing housing to newly admitted military personnel. This means that when a serviceman becomes a participant in the NIS, he cannot be classified as needing living space under other government programs.

Expert opinion

Kozlov Andrey Kirillovich

Lawyer with 10 years of experience. Specialization: criminal law. More than 3 years of experience in developing legal documentation.

Such measures will exclude repeated excess housing provision (an employee must have only one immovable residential property purchased with budget funds).

The legislation also provides for voluntary participation in the NIS. Starting from 2021, a person who has entered the service from the reserve will not be able to be forcibly included in the category of participants in the savings mortgage system without his knowledge.

The only basis for entry will be and will be enshrined in law only by a written, official and, most importantly, voluntary application with a request to be included in the register of military personnel in need of housing.

Amount of savings contributions

The Ministry of Finance introduced a draft law on the federal budget for future years, including 2021, to the State Duma. In accordance with the planned changes, the amount of one savings contribution will be 288 thousand.

410 rubles. In the current year 2019, such a contribution is a little more than 280 thousand.

That is, the increase will ultimately be more than 8.4 thousand (in percentage terms, this is 3%).

A simple calculation allows you to find out that after increasing the contribution, one monthly amount of mandatory payment will be equal to 24 thousand and 34 rubles.

For your information! The increase in the contribution, as well as other measures of state financial support, is explained by indexation aimed at combating annual inflation. In 2021, the inflation rate is expected to be 3.8%.

total amount

It’s clear how much they give as part of a military mortgage now. But there is no information yet about the size of the amounts for 2021, although there are two options for the development of events. The positive is this: due to annual inflation and rising real estate prices, it is planned to increase the allocated amounts.

The negative option is also being considered by experts. According to this scenario, due to a lack of funds in the federal budget, the total amount of military mortgages may, on the contrary, decrease.

And this is explained not only by forced savings, but also by the lack of a tendency for housing prices to rise: prices are still stable, and in some sectors they are even declining.

Bid

At the moment, the rate under the terms of a military mortgage is 9.2 percent per year. It is not reported anywhere what this figure will be in 2021.

Expert opinion

Kozlov Andrey Kirillovich

Lawyer with 10 years of experience. Specialization: criminal law. More than 3 years of experience in developing legal documentation.

But mortgage interest charges are determined taking into account the key rate set by the Central Bank, so if it decreases, then the rates on housing loans are likely to decrease.

Helpful information! On September 6, 2019, the Central Bank of the Russian Federation decided to lower the key rate to 7%. For 2019, this figure before the changes was 7.25%. That is, there is a possibility of a decrease in interest rates on mortgage loans.

Purchasing apartments in buildings under construction

If a serviceman purchases an apartment related to an unfinished building, an escrow account is opened in his name: funds from it will be transferred to the developer only when the construction company fulfills its obligations and delivers the property. This will eliminate unpleasant situations associated with delays in delivery of housing.

Now you know how the principles of military mortgages will change from 2021. Military personnel are expected to undergo changes that they needed to familiarize themselves with.

On the eve of 2021, banks are providing loans to NIS participants at rates in the range of 8.5-10.6%, the maximum amount of a bank loan for one military personnel under the age of 30 is 2.9 million rubles. To date, a number of credit organizations also work with military personnel under the “family mortgage”, “loan for military spouses” and refinancing (on-lending) programs of existing loans.

By order of the President, mortgage rates should aim for 8%, which we hope will be achieved next year.

The indexation of funded contributions over the years of the existence of the NIS has been carried out unevenly, since the percentage included in the budget for financing the system depends on a number of factors. In particular, the forecast values of inflation, the current filling of the budget and the prospects for its filling, the state of the economic sector, etc. are taken into account.

Table “Contributions transferred to the personal account of an NIS participant and their indexation”

As can be seen from the table, in 2021 there was no indexation of contributions, and in some years the amount of indexation was not insufficient to fully cover the needs of the system. The economic crises of 2008–2010 and 2014–2015 also played a role.

Military mortgages require additional financing, which was confirmed at the meeting of the Prime Minister with the Federation Council on February 25, 2021. Funds to fill the system deficit must be allocated from the federal budget over several years with appropriate indexation of contributions.

According to the Defense Committee, it is these measures that will remove the “debt tails” of military personnel.

It is worth noting that for the first time in many years, the key rate of 6.25% is near minimum values, which has a positive effect on lending programs for military mortgages, but at the same time, income from trust management of savings is decreasing. In these conditions, the best strategy is to invest CZH funds in the purchase of apartments in investment-attractive properties.

If the vector of the Central Bank’s monetary policy continues, then the indexation of contributions to the savings-mortgage system will be within 3%, and investment income will be no more than 5-6%, which is less than the increase in real estate prices.

The Russian government has developed a program to provide military personnel with their own housing. Previously, real estate was issued to military personnel only after retirement due to length of service.

To get housing, you had to wait in line, which could take years. In 2007, the NIS program was developed, which allows you to buy real estate without waiting for the age of dismissal.

I got an apartment with a military mortgage. Soon there will be 20 calendars and I’m going to quit.

After dismissal, the credit schedule is designed for another 5 years. As I understand it, the burden of paying the bank will fall on me upon dismissal on the usual grounds (expiration of the contract).

The question is: if you manage to resign with 20 years of service under the “limited service” clause, who in this case will bear the burden of payments to the bank during these 5 years: on me or on the state? Thank you.

You understand correctly. If you resign under this category, the state will have to pay.

Expert opinion

Davydov Dmitry Stanislavovich

Deputy Head of the Military Commissariat

See Federal Law “On the savings and mortgage system of housing for military personnel” dated 08/20/2004 N 117-FZ (latest edition), Art. 15

You can use savings, but you will still have to pay for the remaining 5 years. The right to use savings for housing provision is provided for in Article 10 of the Federal Law of August 20, 2004 No. 117-FZ “On the savings and mortgage system for housing provision for military personnel.”

Art. 10 The basis for the emergence of the right to use savings accounted for in the participant’s personal savings account in accordance with this Federal Law is: 1) the total duration of military service, including in preferential terms, twenty years or more

;

2) dismissal of a serviceman whose total duration of military service is ten years or more: b) for health reasons - in connection with his recognition by the military medical commission as limitedly fit for military service;

Hello, I clarify that the legal regulation of the functioning of the savings-mortgage system is carried out in accordance with the Federal Law of the Russian Federation of May 27, 1998 N 76-FZ “On the status of military personnel” and the Federal Law of the Russian Federation of August 20, 2004 N 117-FZ “On savings- mortgage system for housing support for military personnel”, Rules for providing targeted housing loans to participants in the savings-mortgage system for housing support for military personnel.

According to paragraph 2 of Art. 3 of the Federal Law of August 20, 2004 N 117-FZ “On the savings-mortgage system of housing for military personnel”, participants in the savings-mortgage system are military personnel - citizens of the Russian Federation, performing military service under a contract and included in the register of participants.

Targeted housing loan is funds provided to a NIS participant on a repayable and gratuitous or repayable basis in accordance with the Federal Law (clause 8 of Article 3 of Federal Law N 117-FZ).

According to Art. 14 of the Federal Law “On the savings-mortgage system of housing support for military personnel”, the source of provision of a targeted housing loan to a participant in the savings-mortgage system is the savings for housing support recorded on the participant’s personal savings account.

From the date of provision of a targeted housing loan, income is recorded on the participant’s personal savings account based on the balance of savings for housing recorded in this account.

A targeted housing loan is provided for the period during which a participant in the savings-mortgage system undergoes military service.

Article 11 of the Federal Law of the Russian Federation “On the savings and mortgage system of housing for military personnel”, a NIS participant has the right to: use the funds specified in paragraphs. 1 and 3 hours

1 tbsp. 4 of this Federal Law, for the purpose of acquiring residential premises or residential premises into ownership or for other purposes after the right to use these funds arises; use a targeted housing loan for the purposes provided for in Part.

1 tbsp. 14 of this Federal Law; annually receive from the federal executive body in which he is serving in military service information about the funds recorded in his personal savings account.

The NIS participant is obliged to: return the provided targeted housing loan in cases and in the manner determined by this Federal Law; notify the authorized federal body of his decision regarding the funds accumulated in his personal savings account upon dismissal from military service. Receipt by the participant of the funds specified in Part.

1 tbsp. 4 of this Federal Law, or the direction by an authorized federal body to the participant’s creditor of funds from a targeted housing loan for the purposes provided for in paragraph.

2 hours 1 tbsp.

14 of this Federal Law is the fulfillment by the state of its obligations to provide housing for military personnel.

According to paragraph 1 of Art.

15 of the Federal Law of the Russian Federation “On the savings-mortgage system of housing provision for military personnel”, repayment of a targeted housing loan is carried out by the authorized federal body if the participant in the savings-mortgage system who received the target housing loan has the grounds specified in Art. 10 of this Federal Law, as well as in the cases specified in Art.

This is important to know: Do you need a military ID for a mortgage?

12 of this Federal Law.

In accordance with Decree of the President of the Russian Federation of April 20, 2005 N 449 “Issues of the savings and mortgage system of housing provision for military personnel,” the functions of the authorized federal executive body ensuring the functioning of the NIS are assigned to the Ministry of Defense of the Russian Federation.

In pursuance of the said Decree, by Decree of the Government of the Russian Federation of December 22, 2005 N 800, to ensure the functioning of the NIS and the implementation by the Ministry of Defense of the Russian Federation of the functions of the authorized federal executive body ensuring the functioning of the said NIS, the federal state institution “Federal Administration of the Savings and Mortgage System of Housing for Military Personnel” was created ( "Rosvoenipoteka").

Based on Part 3 of Art. 9 of the Federal Law of August 20, 2004 N 117-FZ, one of the grounds for the exclusion of a serviceman by the federal executive body, in which federal law provides for military service, from the register of participants is his dismissal from military service.

After the dismissal of a participant in the savings-mortgage system from military service and in the cases provided for in Article 12 of this Federal Law, the participant’s personal savings account is closed and his participation in the savings-mortgage system is terminated (Part 2 of Article 13 of the Federal Law of August 20, 2004 . N 117-FZ).

In accordance with clause 63 of the Rules for providing targeted housing loans to participants in the savings and mortgage housing system for military personnel, as well as repayment of targeted housing loans, approved by Decree of the Government of the Russian Federation of May 15, 2008 N 370 after receiving information from the federal executive authorities about the exclusion of the participant from of the register of participants, the authorized body terminates the repayment of obligations under the mortgage loan.

Thus, it should be concluded that if a participant is excluded from the register of participants, NIS must pay off the debt remaining under the mortgage loan agreement on its own.

So, according to the Federal Law “On the savings and mortgage system of housing for military personnel” dated August 20, 2004 N 117-FZ (latest edition), Art. 15 there are various cases of dismissal from military service and each of them has its own mechanism for stopping the military mortgage.

TsZHZ (targeted housing loan) is that part of the amount that accumulates in the personal savings account of a military member participating in the NIS, and which the state, represented by FGKU Rosvoenipoteka, transfers to the bank (or the seller, if the purchase occurs without borrowed funds). Depending on the reason for dismissal, the employment center may become gratuitous (i.e.

it does not need to be returned) or must be completely returned to the state.

Expert opinion

Davydov Dmitry Stanislavovich

Deputy Head of the Military Commissariat

In case of a full return, the serviceman is given 10 calendar years with an approved payment schedule to return the TsZZ, and interest will be charged according to the Central Bank refinancing rate.

Monthly payments are made by the state to the bank account where the mortgage was taken out. Calculated as 1/12 of annual savings contributions. Depending on the reason for dismissal, they will have to be returned in full, like the CZZ, with interest at the refinancing rate, or they will become free of charge.

Due to the high age of 20 years and preferential dismissal due to health, the burden of paying the mortgage lies with the state.

Dear Kirill, Vladimir!

With a Military mortgage, the payer of the mortgage is the Ministry of Defense of the Russian Federation (Federal Law “On the savings-mortgage system of housing for military personnel” dated August 20, 2004 N 117-FZ).

If you are discharged from the RF Armed Forces for health reasons - due to the military medical commission recognizing you as partially fit for military service, unfortunately, paying the mortgage for the last 5 years is assigned to you.

Good luck to you Vladimir Nikolaevich

Good evening, Kirill!

If you have 20 years of service, then it doesn’t matter on what grounds you resign.

. According to Art. 10 Federal Law of August 20, 2004 N 117-FZ “On the savings and mortgage system of housing for military personnel”

The balance of the mortgage will be repaid at the expense of Rosvoenipoteka, you will be paid additional payments with which you will cover the balance of the mortgage.

3. In the event that a participant in the savings-mortgage system acquires housing during the period of military service at the expense of part of the savings using a targeted housing loan and repays the said loan upon the dismissal of the participant by decision of the federal executive body in which he served in military service to exclude the participant from register of participants and on the basis of its report (application), the authorized federal body ensures that the participant is provided with the balance of cash savings and closes the participant’s personal savings account.

The answers are contradictory. In the end it is not clear. Is there any judicial practice?

According to paragraph 1 of Art.

15 of the Federal Law of the Russian Federation “On the savings-mortgage system of housing provision for military personnel”, repayment of a targeted housing loan is carried out by the authorized federal body if the participant in the savings-mortgage system who received the target housing loan has the grounds specified in Art. 10 of this Federal Law, as well as in the cases specified in Art.

12 of this Federal Law.

After the dismissal of a participant in the savings-mortgage system from military service and in the cases provided for in Article 12 of this Federal Law, the participant’s personal savings account is closed and his participation in the savings-mortgage system is terminated (Part 2 of Article 13 of the Federal Law of August 20, 2004 . N 117-FZ).

What is NIS

The savings mortgage system (NMS) involves making monthly transfers to the individual account of a serviceman to further improve his living conditions. It opens automatically after 3 years of military service or at the request of the employee. The amount of deductions does not depend on the rank, period and place of service of the program participant.

After joining the program, funds accumulate in the serviceman’s account, which can be used to purchase housing. In 2021, there are 2 ways to purchase real estate:

- Wait until the required amount is collected in the account (the maximum possible amount of savings in 2021 is 2.4 million rubles) and buy a home.

- Without waiting for the required amount to be collected, apply for a military mortgage at the bank. The savings available in the NIS account can be used to pay the down payment.

In the second case, payments on a military mortgage will be made not by the borrower himself, but from funds from the Federal Budget.

Money in the account works the same way as in a simple deposit. A serviceman can receive additional income in the form of annual interest on the amount placed on the NIS account. This additional income can also be used to purchase a home or make regular monthly mortgage payments.

Previously, contributions to an individual account were made once a month, but starting in 2021, payments became annual. They are transferred until March 20 of the current year. The amount of funds allocated to an employee under the NIS program is constantly increasing, since accruals are subject to annual indexation.

The question often arises: can a military man dispose of his savings in the NIS at his own discretion. To answer this question, you should study Art.

10 No. 117 – Federal Law “On the savings and mortgage system of housing for military personnel.” This regulatory legal act explains that the following categories of participants can spend NIS funds for personal purposes:

- Military personnel who have served in the army for 20 years or more;

- Certain categories of participants who have served in the RF Armed Forces for at least 10 years.

The second group includes military personnel who left the army after 10 years of service for the following reasons:

- A change in health condition that resulted in the military being declared unfit for service;

- Family circumstances;

- Organizational staffing activities.

This also includes military personnel who retired due to reaching the age limit for military service.

How a military mortgage is paid when a serviceman is discharged: different situations

If a citizen - NIS participant - retired from the army, the further fate of his military mortgage will depend on the following parameters:

- Reason (ground) for leaving the armed forces.

- Duration of military service (length of service).

- The fact of the intended use (mastery) of NIS funds by a military personnel.

- Existence of debt to the creditor bank on a mortgage (target housing loan).

Dismissal from the army after 20 years of service

If a citizen purchased housing with mortgage funds, but retired from the army after serving at least 20 years (taking into account preferential calculation of length of service), repayment of this loan is carried out according to the following rules:

- If the mortgage loan is paid in full by the time of separation, the NIS funds provided do not need to be returned to the government. In addition, monthly payments made by Rosvoenipoteka for a military serviceman are also non-refundable. In order to remove the mortgage collateral issued in favor of the state from the purchased housing, the leadership of the military unit sends the appropriate information to the Rosvoenipoteka division.

- If a citizen has a military mortgage debt to a creditor bank (there were not enough funds from the NIS account), he pays it off with his own funds. In such cases, the lending bank often transfers the borrower to a regular mortgage, changing the interest rate. The mortgage issued in favor of the creditor bank is removed from the purchased apartment upon the complete settlement of this debt.

If a citizen left the army after 20 years of service and bought residential premises with NIS funds without obtaining a mortgage, the following rules apply:

- Funds provided to a service member are non-refundable. The mortgage on housing is removed in the usual manner - data on the individual’s right to the corresponding savings is transferred to the Rosvoenipoteka division.

- If there are savings left on the NIS personal account, the citizen can receive these funds by sending a corresponding report to the commander. This money is transferred by Rosvoenipoteka and can be used by individuals for personal purposes.

Dismissal of a military personnel on preferential terms after 10 years of service

If a person left the army for good reasons (age limit, family circumstances, deteriorating health, general military service), having served at least 10 years, the following rules for closing a military mortgage apply:

- If the loan is fully repaid, the savings in the personal account and the monthly payments made are not returned to the state. Removal of the deposit from a purchased apartment is carried out in the usual way - information is transferred from the unit to Rosvoenipoteka.

- If the mortgage loan is not paid in full, the service member is responsible for repaying the debt on his own. A dismissed citizen has the right to use additional funds from Rosvoenipoteka. They are paid for years of service, missing up to 20 years of service. The creditor bank removes the collateral from the purchased property after the debt is closed.

This is important to know: Is it worth taking out a military mortgage?

If a retired serviceman bought an apartment without obtaining a mortgage using savings in a personal NIS account, the following conditions apply:

- The accumulated funds are not returned to the state. The deposit is removed by sending a notification to Rosvoenipoteka (it is sent by the command of the military unit).

- If a person receives additional funds, he draws up a report of proper content (supporting documentation is attached to it). This money is used by the citizen at will.

Retirement from the army with length of service not exceeding 10 years

If a person left the military service without serving 10 years, but purchased housing through a military mortgage, the following rules apply:

- Funds from a targeted housing loan, including the start-up fee and monthly payments made by Rosvoenipoteka for a military personnel, are subject to repayment within 10 years after retirement. The deposit on the purchased apartment is removed upon full repayment of the mortgage funds.

- If the borrower still has a mortgage debt to the lending bank, he pays it off independently, using his own funds.

If a discharged serviceman bought housing with NIS funds without a mortgage, he returns the resulting savings to the state within a ten-year period.

Retirement from the army due to failure to fulfill the terms of the contract

This option of dismissal is considered negative from the point of view of the military mortgage. If a person who bought an apartment with NIS funds was dismissed from the army for non-compliance with the terms of the military contract, the following requirements apply:

- Over the course of 10 years, the dismissed citizen returns to the state the entire amount of the loan received with accrued interest. If he does not do this, he will lose the acquired living space.

- If there is still a mortgage debt to the creditor bank, the serviceman pays it off on his own.

Indexation of military mortgages

The amount of funds allocated to military personnel under the NIS program is constantly increasing. This is achieved due to the fact that they are indexed once a year.

Over the entire period of the program, the indexation of accruals was not carried out only in 2021, which caused some military personnel to have difficulties making monthly payments on military mortgages.

Increase in contributions under the NIS program by year

Below is a table that clearly shows how, thanks to indexation, the size of transfers to NIS participants changed:

| Year | Amount of transfers, in rubles |

| 2019 | 280009,7 |

| 2018 | 268465,6 |

| 2017 | 260141 |

| 2016 | 245880 |

| 2015 | 245880 |

| 2014 | 233100 |

| 2013 | 222000 |

| 2012 | 205200 |

| 2011 | 189800 |

| 2010 | 175600 |

| 2009 | 168000 |

| 2008 | 89900 |

| 2007 | 82800 |

How to withdraw savings from a military mortgage upon early dismissal

Expert opinion

Davydov Dmitry Stanislavovich

Deputy Head of the Military Commissariat

The need for early dismissal arises for various reasons. If a NIS participant did not complete his service due to health reasons and a military mortgage was not issued, he can withdraw his savings if he has more than 10 years of service.

The procedure for paying additional funds for a military mortgage takes into account the reasons for dismissal and length of service. Those dismissed on preferential terms can count on such payments if they have more than 10 years of experience.

Advantageous factors are:

- Organizational and staffing measures;

- Medical indications;

- Family circumstances;

- Age limit.