Welcome! Today you will learn what a mortgage is and can calmly approach the signing of this important document. In fact, everything is simple with this document, you just have to figure it out.

So, a mortgage on an apartment is a valuable document confirming the right of the owner of the paper to the property encumbered with the mortgage. In other words, the mortgage confirms the bank’s collateral rights when applying for a mortgage. This security is a guarantee of the interests of the financial institution, and it is issued by the bank, usually at the time of signing the mortgage agreement.

The requirements for this security are described in the mortgage law and are regulated by this document.

Russian legislation gives banks the right to receive interest on each mortgage issued. But in the event of a threat of bankruptcy, ruin or great financial need, the mortgages held by the bank can save it. This does not mean that the bank will sell all its collateral and pocket the money, no. Mortgages merely insure a financial organization, as they carry the potential for profit. But more on that later.

A mortgage for a secondary home must be issued with the signing of the mortgage and its registration.

As a standard, a jar can be pawned:

- Apartment;

- Plot of land;

- Private house with land;

- Any industrial buildings and structures.

The mortgage on the apartment must be kept by the owner - that is, by the bank that issued the loan to you. The borrower receives the right to take back this document only when he fully repays the mortgage debt.

Rosreestr

The rights of the mortgagee under the obligation secured by the mortgage and under the mortgage agreement can be certified by the mortgage in accordance with Article 13 102-FZ “On mortgage (mortgage of real estate)” dated July 16, 1998.

A mortgage is a registered security that certifies the following rights of its legal owner: the right to receive fulfillment of monetary obligations secured by the mortgage, without providing other evidence of the existence of these obligations; right of lien on property encumbered with a mortgage.

The obligors under the mortgage are the debtor for the obligation secured by the mortgage and the mortgagor.

Drawing up and issuing a mortgage is not allowed if:

1) the subject of the mortgage is:

enterprise as a property complex;

the right to lease the property listed in this subclause;

2) a mortgage secures a monetary obligation, the amount of debt for which is not determined at the time of concluding the agreement and which does not contain conditions allowing this amount to be determined at the appropriate time.

In the cases provided for in this paragraph, the terms of the mortgage in the mortgage agreement are invalid.

The mortgage is drawn up by the mortgagor, and if he is a third party, also by the debtor for the obligation secured by the mortgage.

The mortgage is issued to the original mortgagee by the rights registration authority after state registration of the mortgage. A mortgage may be drawn up and issued to the mortgagee at any time before the termination of the obligation secured by the mortgage. If the mortgage is drawn up after the state registration of the mortgage, a joint application of the mortgagee and the mortgagor is submitted to the rights registration authority, as well as a mortgage, which is issued to the mortgagee within one day from the moment the applicant applies to the rights registration authority.

The debtor under the obligation secured by the mortgage, the mortgagor and the legal owner of the mortgage may, by agreement, change the previously established terms of the mortgage.

State registration of an agreement to change the contents of a mortgage with an indication in the text of the mortgage itself of the agreement as a document that is an integral part of the mortgage must be carried out as registration of the transaction within one day from the moment the applicant contacts the rights registration authority with the presentation of the original of the mortgage and the agreement to change contents of the mortgage.

An entry in the mortgage on a registered agreement to change the content of the mortgage, indicating the date and number of its state registration, must be made by the state registrar, certified by his signature and sealed by the rights registration authority. These actions are carried out free of charge.

In the event of cancellation of the mortgage and at the same time the issuance of a new mortgage, together with an application for making changes to the records of the Unified State Register of Real Estate, the mortgagor and the mortgagee transfer to the rights registration authority the mortgage to be canceled and a new mortgage, which is handed to the mortgagee instead of the canceled mortgage.

The canceled mortgage is stored in the archives of the rights registration authority until the mortgage registration record is redeemed.

For the purpose of state registration of an agreement to change the content of a mortgage, the following are entered in the register of rights to real estate:

record of the transaction - state registration of the agreement to change the contents of the mortgage;

changes to the record of restriction (encumbrance) (in the record of restriction (encumbrance), if the subject of the mortgage is more than one piece of real estate (for example, a land plot and a residential building located on it).

The completed state registration of an agreement to change the contents of the mortgage is certified by affixing a stamp of the registration inscription on the documents to the agreement (a special registration inscription if the agreement was submitted in the form of an electronic document). The lender has the right to transfer the rights to the mortgage to any third parties. Inscriptions on the mortgage that prohibit its subsequent transfer to other persons are void.

Registration of the legal owner of the mortgage is carried out by filling out a new record of restriction (encumbrance) - state registration of the mortgage in favor of the new mortgagee.

The new entry on the restriction (encumbrance), with the exception of information about the mortgagee, contains information similar to the information in the entry on the restriction (encumbrance) in which the original mortgagee or the previous legal owner of the mortgage was indicated.

The new entry on the restriction (encumbrance) in relation to the mortgagee indicates the details of the person who applied to make a registration entry about him as the legal owner of the mortgage. In relation to the basis documents, the details of the document basis for entering this information are additionally indicated.

rosreestr.ru

Valuation of collateral property

To clarify the real value of the real estate that serves as security for the mortgage agreement, it is necessary to order an appraisal.

Without such a procedure, as Art. 13 clause 4 of the Law of the Russian Federation No. 102-FZ , registration and issuance of a mortgage is impossible if the value of the object in monetary terms has not been established or its determination is difficult.

Registration of a mortgage at the MFC

Registration of a mortgage at the MFC

With the deteriorating economic climate and the advent of a recessionary cycle in the economy, the real estate market has fallen on hard times. The population simply does not have enough money to buy an apartment, and until recently the interest on the loan was simply extortionate.

Accordingly, the government of the country took measures aimed at maintaining stability in the economy. In particular, a gradual and systematic reduction in the rate of the Central Bank of Russia was carried out, which made obtaining loans more accessible.

Currently, there is a slow and uncertain recovery in the real estate market. However, most transactions for the purchase of housing are carried out using funds from mortgage loans.

And here many difficulties arise - the law establishes that all transactions with real estate must be registered with Rosreestr. Transactions involving a mortgage require registration of not only the agreement, but also the mortgage on the loan. You can register this paper at the offices of the Multifunctional Center.

Registration of a mortgage at the MFC

There are two options here - either you personally go to Rosreestr, or you contact the MFC, which acts as an intermediary between you and the department. Before visiting, we recommend making a pre-registration, since citizens who are pre-registered come to the employee at the appointed time without queuing. This will allow you to save your nerves and time.

It is important! The procedure takes from five days to two weeks, depending on the specific case, so it is better to check the execution time with an MFC specialist by calling the hotline number.

List of required documents for registration of a mortgage

To complete the necessary paperwork, you should submit the following package of documents to the department of the multifunctional center:

- passport of a citizen of the Russian Federation with a registration mark. Registration must be at the same address as your place of residence;

- real estate valuation report. Appraisers are now a dime a dozen, and there are scammers among them, therefore, it is necessary to ask the financial institution about the specialists whose opinion it trusts;

- cadastral passport. You can also apply for it through the MFC;

- contract and transfer deed for real estate;

- a copy of the decision of the local government to put the facility into operation;

- If you are married, then in addition to the listed documents, you will also be required to provide a Marriage Certificate. And sometimes the consent of the spouse, certified by a notary.

Similar articles:

Dear visitors!

Do you have any questions? Question to a lawyer with a guarantee of a quick answer? We understand that each case is unique and we are not describing a complete solution to your problem.

To quickly resolve your problem, we recommend contacting experienced and qualified lawyers on our website.

uslugi-mfc.ru

Registration of a mortgage at the MFC

Are a mortgage agreement and a mortgage note the same thing?

How to apply for a mortgage

Issuance and registration of a mortgage in Rosreestr

What happens to the mortgage after the mortgage is paid off?

Are a mortgage agreement and a mortgage note the same thing?

Definitions of the concepts “mortgage agreement” and “mortgage” are given in the Law “On Mortgage...” dated July 16, 1998 No. 102-FZ (hereinafter referred to as Law No. 102-FZ):

- A mortgage agreement is concluded between the mortgagor (debtor) and the mortgagee (creditor). Its object is to provide the creditor with a preemptive right to satisfy monetary interests in the event of the debtor's failure to fulfill his obligation. The interests of the creditor will be satisfied through the sale of the pledged property.

- Mortgage in accordance with clause 2 of Art. 13 of Law No. 102-FZ is a security that certifies the above-mentioned pre-emptive right of the pledgee. A mortgage can be documentary, and from July 1, 2018, non-documentary (issued in electronic form). Details in the article What is a mortgage on an apartment?

Thus, the mortgage is a document derived from the mortgage agreement. It can be either formalized or not.

How to apply for a mortgage

There is no form of mortgage approved by the normative act; it is drawn up by the mortgagor (debtor) taking into account the requirements of Art. 14 of Law No. 102-FZ. According to this norm, the mortgage must contain:

- the word "mortgage";

- information about the pledgor: full name and passport details of an individual or name and address of a legal entity;

- the same information about the first mortgage holder;

- information about the obligation: the basis for its occurrence, details of the contract;

- amount of debt with interest;

- description of the pledged property;

- information about state registration of mortgages, etc.

The mortgage may contain other information at the discretion of the parties, but the information specified in Art. 14 of Law No. 102-FZ must be mandatory. Otherwise, the mortgage will not be considered as such and will not be transferred to the mortgagee.

A mortgage as a security can change the owner, information about this is entered into it itself, the transfer of rights under an electronic mortgage occurs by making an entry in the securities account.

If there is not enough space on the document itself to make an entry, an additional sheet is attached to the mortgage (Clause 3, Article 14 of Law No. 102-FZ).

Information about the owner of the mortgage may be registered by a government agency.

Issuance and registration of a mortgage in Rosreestr

So, the mortgage is made by the debtor. He submits this document to Rosreestr simultaneously with a joint application for mortgage registration (Clause 3, Article 20 of Law No. 102-FZ). An electronic mortgage is drawn up by filling out a special form on the Rosreestr website or on the government services portal, and is signed with an enhanced qualified electronic signature of the mortgagor and the mortgagee. Other documents are provided in the form of electronic documents

The lender receives the mortgage in hand immediately after making an entry about the mortgage in the Unified State Register of Real Estate, and the electronic mortgage is transferred for storage to the depository.

He has the right to request a mortgage later, until the debt is repaid. Then the mortgage is issued to the mortgagee within a day from the moment of application (clause 5 of article 13, clause 3 of article 13.3 of law No. 102-FZ).

Registration of a documentary mortgage in Rosreestr, or rather, entering information into the Unified State Register of Real Estate about its holder, is carried out at the request of the latter (clause 1 of Article 16 of Law No. 102-FZ).

The mortgagee must notify the debtor of the entry made in the Unified State Register of Real Estate, who continues to make payments until the debt is repaid in full or until he receives notice of the assignment of rights under the mortgage.

If the mortgage has a new owner, information about him is entered into the Unified State Register of Real Estate within 1 day from the date of the applicant’s application (clause 3 of Article 16 of Law No. 102-FZ). The debtor must also be notified of this.

It is possible to submit documents for registration of the transfer of rights under a documentary mortgage through the MFC, commonly referred to as registration of the mortgage in the MFC. This follows from the special rules on registration of a pledge (Part 10, Article 53 of the Law “On State Registration of Real Estate” dated July 13, 2015 No. 218-FZ, hereinafter referred to as Law No. 218-FZ) and the general rules on filing an application for registration (clause 1 part 1 article 18 of law No. 218-FZ).

What happens to the mortgage after the mortgage is paid off?

According to paragraph 2 of Art. 17 of Law No. 102-FZ, upon full repayment by the debtor of his debt, the mortgagee must immediately return the mortgage to him. In this case, the document must contain an inscription indicating the fulfillment of the obligation - full or partial.

The inscription contains (clause 2 of article 25 of law No. 102-FZ):

- the words “fulfillment of an obligation”;

- execution date;

- owner's signature;

- owner's stamp, if available.

If there is no such inscription on the mortgage and it is not returned to the mortgagor, it will be considered that the debt has not yet been repaid until proven otherwise (Clause 3 of Article 17 of Law No. 102-FZ).

A record of mortgage repayment is made in the Unified State Register of Real Estate within 3 days from the date of receipt of the application. Simultaneously with the repayment of the entry, the mortgage is canceled by affixing the stamp “REDEMPTED” (Clause 3, Article 25 of Law No. 102-FZ). When the mortgage record is redeemed, an application for cancellation of the electronic mortgage is not necessary (Clause 6, Article 13.4 of Law No. 102).

***

Thus, Rosreestr, leading the Unified State Register of Real Estate, registers the transfer of ownership of real estate and its encumbrance in the form of a mortgage.

However, the mortgagee may request to make a record of the existence of a mortgage in the Unified State Register of Real Estate. He can send such an application in any way convenient for him, including by submitting it to the MFC.

rusjurist.ru

Why do you need a mortgage for an apartment and what does it look like?

A mortgage note is a security document confirming the transfer of an apartment as collateral to the bank. If the borrower stops paying the loan, the bank can do 2 things:

- Repossess and sell the mortgaged property.

- Sell or transfer a mortgage to another bank.

The subject of collateral can be:

- Apartment.

- A private house.

- Non-residential premises.

- Country cottage area.

- Industrial buildings and structures.

Expert opinion

Alexander Nikolaevich Grigoriev

Mortgage expert with 10 years of experience. He is the head of the mortgage department in a large bank, with more than 500 successfully approved mortgage loans.

Until the mortgage is paid, the mortgaged property is under the bank's encumbrance. After the loan is fully repaid, the mortgage is canceled and the owner can dispose of the property at his own discretion. If the apartment is pledged, the borrower must ask the bank’s consent to carry out any transactions. He will not be able to sell, donate or exchange the apartment without the bank’s permission.

Why do you need a mortgage for an apartment?

- The borrower who takes out a pledge receives more favorable lending conditions. This does not apply to all banks.

- The bank receives a money back guarantee. If the borrower stops paying the loan, the document allows the bank to sell the mortgaged property and return the money.

- The bank may attract third-party investments. The law allows the lender to sell mortgages to other banks and make money from it. The conditions for the borrower do not change.

What should the document contain?

The requirements for the content of a mortgage and the procedure for its execution are prescribed in Chapter 3 of Federal Law No. 102 “On mortgage (real estate pledge).” There is no single form for this document.

By law, this paper must contain:

- Name and identification number. The name must include the word “Mortgage”. The number is usually indicated in the header of the document.

- Information about the bank (mortgagee). Legal address, full name, license of a banking institution, checkpoint, tax identification number.

- Information about the borrower (mortgagor). Individuals indicate their full name, registration address, passport details, SNILS. For legal entities, you must provide the full name of the organization, legal address, TIN, KPP. In rare cases, the mortgagor is not the borrower, but another person. Then indicate his data.

- Information about the mortgage agreement. Indicate the document number, date of registration, loan amount, repayment schedule, monthly payment amount, interest. If the loan is taken out in a foreign currency, it is necessary to register the conversion rate of this currency into rubles. This is necessary to correctly determine the cost of the loan and interest. Pay special attention to this point - violation of the terms of the agreement gives the bank the right to seize the collateral.

- Description of the collateral property. Indicate the address, area of the property, number of rooms, cadastral passport number.

- Assessed value. The document also states the estimated value of the property, indicated by an independent expert.

- The presence of other encumbrances on the object (rent, lease, arrest) . If there are no encumbrances, write this down.

- Stamp and signature. Signatures of the parties, seals (for banks and legal entities), date of preparation of the document.

Attention! You sign a document that will allow the bank to take your apartment if the mortgage agreement is violated. Carefully check the contents of the mortgage for errors. Make sure that the data matches the contents of the loan agreement. If further disagreements arise, the court will rely on the mortgage.

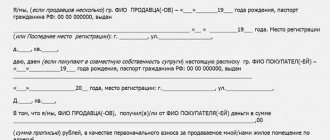

Example of a mortgage form

You can see what a mortgage note looks like in the visual preview window below. You can follow this link and open it on your computer in Word.

One more example:

Rosreestr

In accordance with Article 13 of the Federal Law of July 16, 1998 N 102-FZ “On Mortgage (Pledge of Real Estate)” (hereinafter referred to as the Mortgage Law), the rights of the mortgagee under the obligation secured by the mortgage and under the mortgage agreement can be certified by the mortgage.

A mortgage is a registered security certifying the following rights of its legal owner:

· the right to receive fulfillment of monetary obligations secured by a mortgage, without providing other evidence of the existence of these obligations;

· right of pledge on property encumbered with a mortgage.

As a general rule, according to Art. 25 of the Mortgage Law, the mortgage registration record is canceled on the basis of a joint application of the mortgagor and the mortgagee.

However, if there is a mortgage record issued to the mortgagee, it can be redeemed at the request of one party: the owner of the mortgage or the mortgagor with the simultaneous submission of a mortgage note containing a note from its owner about the fulfillment of the obligation secured by the mortgage in full.

Such a mark must include words about the fulfillment of the obligation and the date of its execution, and must also be certified by the signature of the owner of the mortgage and certified by his seal (if any), if the owner of the mortgage is a legal entity.

When the mortgage registration record is redeemed in connection with the termination of the mortgage, the mortgage is canceled, after which it is transferred to the person previously obligated on it upon request.

If residential premises were purchased or built using credit funds and partially using savings for housing provision for military personnel provided under a targeted housing loan agreement (Federal Law “On the savings-mortgage system for housing provision for military personnel”), an additional application from the Federal State Institution “Rosvoenipoteka” must be submitted.

The mortgage record is repaid within three working days from the moment the relevant applications are received by Rosreestr.

In addition, the mortgage can be repaid on the basis of a joint application of the mortgagor and the mortgagee, by decision of a court or arbitration court.

Thus, to redeem the mortgage registration record, the provision of documents other than applications and the mortgage is not required.

In the event of liquidation of the mortgagee - a legal entity, the registration record of the mortgage is canceled on the basis of the application of the mortgagor and an extract from the unified state register of legal entities, confirming the entry into the specified register of an entry on the liquidation of this legal entity.

The Rosreestr Office for the Altai Territory draws attention to the fact that no state duty is charged for mortgage repayment.

| T.V. Afanasyeva, head of the department for registration of rights, restrictions (encumbrances) and provision of information on registered rights of the Rosreestr Office for the Altai Territory |

rosreestr.ru

Storage

The only copy of the document is kept by the owner (mortgagee).

The original owner is the bank, which has the right to sell the rights to the pledge , then the paper has a new owner. This procedure is allowed to be carried out as many times as desired, and storage is always taken over by the next owner.

Clause 8 art. 13 No. 102-FZ states that a document can be transferred for storage to a depository .

Registration of mortgage in Rosreestr

The procedure for registering ownership of an apartment with a mortgage in 2018

It is advisable to sign them in the presence of the registrar; receipt of payment of the state duty for registering the transfer of ownership; contract of sale; title and title documents for the property presented by the seller; a pledge agreement concluded with a bank under which an encumbrance on real estate is registered; cadastral passport for the apartment; extract from the house register; certificate of absence of debt for utility services in relation to the registered apartment; written consent of the guardianship authorities.

State registration of a new mortgage owner

In addition, according to paragraph 1 of Article 16 of the Law on Mortgage, registration of the legal owner of the mortgage in the Unified State Register of Rights to Real Estate and Transactions with It (hereinafter referred to as the Unified State Register) as a mortgagee is his right, not his obligation. Clause 4.2 of Article 20 of the Mortgage Law establishes that the entry into the Unified State Register of Information about the new mortgagee as a result of the transfer of the mortgage is carried out at the request of the new owner of the mortgage.

Registration of mortgage in Rosreestr

in the event that the land plot on which the apartment building and other real estate objects included in such a building are located was not formed before the entry into force of the Housing Code of the Russian Federation, on the basis of a decision of the general meeting of owners of premises in the apartment building, any person authorized by the said meeting has the right to apply to state authorities or local authorities with an application for the formation of the land plot on which the apartment building is located.

State registration of a mortgage agreement

So, the primary source (Article

10 of the said legislative act) tells us the following:

“The mortgage agreement is subject to mandatory state registration and is recognized as coming into force from the moment of such registration.” But wait, well-read citizens will say now, what about the newly created Article 334.1 of the Civil Code of Russia? Indeed, according to the changes that came into force on July 1, 2014, registration of a real estate pledge agreement, which is a mortgage, is not the basis for the emergence of a pledge.

Procedure for registering a mortgage in Rosreestr, deadlines

An important point is the payment of state duty.

This obligation rests with the person providing security for the mortgage. The state duty is paid on preferential terms if the obligation arose due to the operation of a certain law. If the general rules are followed, then the state duty is paid in full. Registration records are maintained according to standard requirements. A document confirming that the state fee has been paid.

A credit agreement secured by a mortgage.

The MFC generally hints that without some kind of power of attorney from the bank (and they don’t know which one, they get confused!) they can suspend registration. Rosreestr itself denies the need for it (this power of attorney) at all!

What if the bank refuses to give it at all? Help with advice, share your experience!

The MFC generally hints that without some kind of power of attorney from the bank (and they don’t know which one, they get confused!) they can suspend registration.

Rosreestr itself denies the need for it (this power of attorney) at all! What if the bank refuses to give it at all?

Help with advice, share your experience!

The editors of BANKIR.RU are not responsible for the opinions and information published in the comments to the materials. The opinion of the authors of published materials does not always coincide with the opinion of the editors. Responsibility for the information and assessments expressed during the interview lies with the interviewees.

When reprinting materials, please publish a link to the Bankir.Ru portal indicating a hyperlink.

The sheets of the mortgage are numbered and sealed by a notary; all sheets of the mortgage form a single whole. An integral part of the mortgage also includes attachments in the form of documents defining the terms of the mortgage or necessary for the mortgagee to exercise his rights under the mortgage. As established by Article 48 of the Mortgage Law, the transfer of rights certified by the mortgage is carried out by means of an endorsement in favor of the next owner of the mortgage, and the simultaneous transfer of the mortgage this person.

Mortgage for an apartment: what a borrower needs to know

So let's get started.

A mortgage is a secured loan; when it is issued, an encumbrance is placed on the purchased property, with the drawing up of a mortgage. The borrower’s other real estate, including a plot of land, can also serve as collateral for the mortgage.

A mortgage is defined as a security. It is issued to the bearer in relation to the property on which the encumbrance is imposed.

myeconomist.ru

Design features

The document is drawn up in 1 copy . Although the form of paper does not have a clear standard, each bank has developed its own basic mortgage structure.

For the loan recipient, this is even more convenient and simpler: by filling out a mortgage according to the proposed model, the borrower can be sure that he has not missed anything.

It is important to carefully check all the data entered into this security, as well as information about housing - the slightest inaccuracy can lead to a refusal by the bank and to problems in the future.

You should not include a plan for repaying the loan and interest in the text of the document: if it is possible to make payments in a larger amount and close the debt early, there will be a discrepancy.

Read our article about how to pay off your mortgage early.

For information on the new procedure for registering a mortgage for a mortgage, watch the video:

Conditions

The document can be issued under the following conditions:

- the mortgagor's identity card is in good order and is valid,

- the object of the transaction is interesting to the bank,

- the property has been assessed, and there is an official conclusion from the appraiser,

- the appraiser is authorized to perform such actions,

- the object is not under arrest, is not an inherited property under the terms of a lifelong inspection agreement, etc. (there are no encumbrances),

- title documents for the object are in perfect order.

When registering a mortgage, the following conditions must be met:

- the collateral apartment should be described in as much detail so that identification does not raise the slightest questions,

- there must be detailed and reliable information about the person issuing this security,

- if the borrower and the owner of the apartment serving as collateral are not the same citizen, then information about the owner must also be included in the mortgage,

- it is important to indicate how the debt is to be repaid and the exact date of full payment,

- be sure to include in the mortgage the full amount of the mortgage loan , as well as the interest rate ,

- if there are co-borrowers, the signature of each of them is required,

- payment details must be included in the mortgage note.

In the registration of a mortgage, the main participants are the one who receives the real estate and the lending bank.

It is important to know that the absence of government registration of proprietary rights to undemarcated land plots will not prevent a financial institution from issuing a loan against them and taking out a mortgage if it wishes.

How a mortgage is registered in Rosreestr - features and nuances

According to the Federal Law “On Mortgage (Pledge of Real Estate)” dated July 16, 1998 No. 102-FZ, registration of a mortgage in Rosreestr is a procedure that must be completed without fail.

When registering a mortgage in Rosreestr, there are a number of subtleties and important nuances - we will talk about this in this article.

How does the procedure for registering a mortgage take place in Rosreestr?

As you know, mortgage lending is a rather lengthy and tedious process. Since it is collateral, when registering, the consumer is required to go through many additional procedures that are related to insurance, assessment of the purchased real estate, imposition and removal of encumbrances.

The requirements of the Civil and Housing Code of the Russian Federation should be observed with special care.

Registration of a mortgage agreement with Rosreestr is the final stage of registration of a mortgage. This is confirmation of a completed transaction at the highest level – state level. The Rosreestr registers encumbrances, as well as the transfer of rights that arise in connection with the donation, purchase and sale of real estate, rent, privatization, and participation in shared construction.

Registration is carried out within a month, but if you need to double-check the authenticity of the documents provided or any additional papers, the process can be extended for another 30 days.

Registration of encumbrances and transfer of rights is entrusted to the territorial bodies of the Federal Service for State Registration, Cadastre and Cartography (registration chambers).

If we turn to clause 2 of Art. 20 of Law No. 102-FZ as amended on 05/07/2013, it says that mortgages by force of law (including those that are conditioned by attracting funds borrowed from a bank for the construction or purchase of housing) are subject to mandatory registration. The procedure starts from the moment an application is submitted by the borrower and a representative of a financial institution or a notary (notary's assistant) who certified the mortgage agreement without paying a state fee.

If the borrower did not use the services of a notary, then the state fee is subject to mandatory payment - it must be attached to the application. In addition, you must attach a copy of the purchase and sale agreement and the original.

If you go to the official website of Rosreestr, you can download a form to fill out an application. The application is also available at Companies House. If you want to save your time standing in line (of course, a representative of a financial institution will not waste his time in line, so you will need to agree on a specific time with him), it is better to make an appointment in advance.

Important point! It is the mortgage, that is, the transfer of real estate as collateral, that is subject to state registration. Starting from 2013, the mortgage agreement and the accompanying real estate purchase and sale agreement are not subject to registration.

If the mortgage loan was issued for the purchase of land or non-residential premises, the registration process will take 14 days. If you register a real estate mortgage for residential purposes, then this procedure is allotted only 5 working days. Take this point into account and do not waste time with registration.

Features of registering a mortgage in Rosreestr

For Rosreest, mortgage is a conditional concept. A mortgage agreement can be drawn up not only between the borrower and a financial institution. For example, if you want to sell real estate in installments, you have the right to place an encumbrance on it until the buyer pays the bills in full.

There are a number of situations when it is not possible to draw up a mortgage agreement. According to the main provisions of Art. 5 of Law No. 102-FZ, the subject of a mortgage cannot be:

- Garden houses in the country;

- Isolated rooms in apartments;

- Buildings in which business activities are carried out;

- Aircraft;

- Sea vessels.

This also applies to the following land plots (if you are taking out a mortgage to purchase a land plot):

- areas owned by the state;

- lands that have not been withdrawn from circulation for any reason and are smaller than the established size;

- are not separated from public land holdings.

Also, a mortgage agreement cannot be concluded if it is impossible and impossible to provide a collateral assessment of the real estate property.

Depending on the form in which the mortgage agreement was concluded (the encumbrance is imposed by the bank AFTER the issuance of the certificate or WHEN concluding the purchase and sale agreement), Rosreestr distinguishes two types of mortgages:

Mortgage by virtue of the contract

This is a rather rare registration option. Its existence is possible with a mortgage, which is issued for the purchase of residential premises in new buildings. In all other situations, the financial institution will not use this option, since the imposition of an encumbrance on the purchased real estate does not occur immediately with the registration of the purchase and sale agreement, but upon the conclusion of an additional mortgage agreement.

In other words, the bank is in a somewhat ambiguous situation when the borrower has received borrowed funds to purchase real estate, but there is no collateral yet.

But in situations where the seller of an apartment expresses a desire to indicate a lower value in the purchase and sale agreement in order to avoid fulfilling obligations to the tax authority, which does not coincide with the assessment of an independent inspector, the issue is resolved in the only way - by issuing a mortgage loan by virtue of the agreement.

In most cases, financial institutions provide up to 3 months for the borrower to provide a certificate of real estate to draw up an additional mortgage agreement.

Until the bank is granted the right of encumbrance, the interest rate on the loan will be inflated - this is how the financial institution seeks to insure possible risks. If we are talking about shared construction, the loan period without collateral will be extended until the house is put into operation.

Mortgage by operation of law

This is the most common type of mortgage registration. If a mortgage is issued by virtue of the law (clause 1.2 of Article 11 of the Federal Law “On state registration of rights to real estate and transactions with it” dated July 21, 1997 No. 122-FZ), the encumbrance on the purchased property will be imposed automatically, simultaneously with the state registration of the purchase and sale transaction agreement.

In the certificate of real estate that you receive, in the “Encumbrance” column there will be a note stating that it was acquired through a mortgage loan and is collateral. There is an important nuance here - keep in mind that the encumbrance WILL NOT be lifted automatically after you have paid your debts to the financial institution in full.

After the mortgage loan is repaid, you will need to visit the territorial state registration office a second time along with an official from the bank to submit an application to remove the mortgage.

In case of applying for a mortgage, there is no need to invite a bank employee; You only need to have with you a mortgage note with the bank’s mark indicating that the obligations have been fulfilled in full. In other words, a mark indicating that the loan has been repaid. You can order a new certificate, which will not have a mark on the existing encumbrance, but for this you will need to pay a state fee. Within three days the encumbrance will be lifted.

This is the main difference between the two types of mortgages described above. In the case of a mortgage by virtue of an agreement, there is no mark on the encumbrance in the certificate, since it is submitted for registration before the conclusion of the mortgage agreement.

Important information! You can obtain information about encumbrances on the apartment if you request an extract from the registration chamber. If you purchase an apartment on your own, then do not forget about this important nuance and check the history of the apartment with special care.

To summarize, I would like to note that the burden that was imposed by a financial institution can be removed from the tenant not only after the mortgage loan has been repaid in full. This can be done by court decision, by additional agreement with the bank. In rare cases, this is possible when the bank ceases to exist and undergoes complete liquidation as a legal entity.

To remove the encumbrance, you should bring an extract from the Unified State Register of Legal Entities to the registration chamber - it will contain a corresponding entry on liquidation.

www.papabankir.ru

How to return or sell a mortgage?

The mortgagor will receive the mortgage back only if he fulfills all obligations under the loan agreement .

And it doesn’t matter whether it happened on time or ahead of schedule.

From this moment, the rights are fully returned to the mortgagor, and after the bank notes that all debts have been repaid, the settled borrower can cancel the mortgage encumbrance on the apartment on the basis of the returned document.

Sample application for removal of encumbrance on an apartment due to full payment of the mortgage.

to sell the mortgage to any person, while both the loan agreement and the right to use the property remain in force for the mortgagor.

In other words, nothing changes except payment details.

Such a security can serve as a means for the bank to exercise its rights in the following ways:

- sale of document,

- sale of collateral share,

- exchange of collateral objects,

- registration of assignment of rights.

Such actions of the bank, as a pledge holder, are legal .

Registration of mortgage in Rosreestr

Mortgage for an apartment: what a borrower needs to know

So why do you need a mortgage when you have a mortgage? Is it just for additional guarantee of loan repayment? Not at all. Mortgage real estate is already de jure the property of the bank, which, in the event of non-repayment of borrowed funds, is free to dispose of it at its own discretion. The whole point is that a mortgage, as a security, has the right to participate in auctions and act as collateral for investment by the creditor bank itself.

Registration of mortgage in Rosreestr

[1] 2.

Registration of a mortgage for an apartment Before registering ownership of an apartment, you must sign a mortgage with the Bank. Rosreestr reported that now physical. persons in Moscow remove the encumbrance through the MFC (Multifunctional Center).

After a conversation with MFC employees and the Rosreestr hotline, there were questions that no one could answer: 1) What exact (!) list needs to be provided to the MFC, for subsequent transfer to Rosreestr - Rosreestr has one list, the MFC has its own (mainly a discrepancy As for some kind of power of attorney from the bank - either for registration, or for repayment of a mortgage - it’s a dark forest, no one really knows anything for sure.

Real estate mortgage

This paper is personal.

It is issued to the buyer of the property and contains information about him. The subject of the agreement and the subject of the collateral value, with a list of cadastral (technical) characteristics.

Terms of debt repayment, due dates for payment of bills. Methods for early repayment of debt.

Sanctions imposed for violation of the specified conditions, the admissibility of termination.

State registration of a mortgage agreement

In essence, you are registering not the legality of the mortgage agreement concluded between you and the credit institution, but the voluntary reduction of the owner’s rights that arose by virtue of this agreement.

An important point: a mortgage can only be registered in relation to real estate whose owner has a certified title to it. A share in construction (for example, if you purchased an apartment in a house under construction) is not yet property, and therefore cannot be the subject of a mortgage.

Contents of the document

The contents of the mortgage are regulated by Art. 14 of Law No. 102-FZ . The name itself must certainly contain the word “mortgage ”.

Mandatory information that must be included in the document includes:

- Full name of the pledgor, details of passport or other identification document,

- the same in relation to the original mortgagor (if the rights are transferred to another mortgagor),

- name and details of the loan agreement,

- Full name of the debtor, if he is not the actual owner of the mortgaged property, and his passport details,

- the amount of the mortgage obligation, with specification of interest,

- maturity dates of mortgage obligations,

- name, address, main characteristics of the mortgaged property,

- the value of the collateral property, confirmed by the appraiser,

- details of the title document for the mortgagor’s ownership of the property transferred as security for the mortgage (if there are registered rights),

- the signature of the person who provided the property to secure the loan, and if this is a third party, then the signature of the debtor,

- data on registration of the mortgage agreement.

It is important to briefly clarify the entire history of the mortgage - who and when was the first mortgagee and subsequent legal successors, if there were replacements, cancellation, restoration, etc.

If there are encumbrances (other than a mortgage), then this must also be reflected in the document.

It follows from the contents that such a document is one-sided , that is, signed only by the pledgor. The form of the document is free, the main thing is that all the necessary information is recorded; adding additional items is not prohibited, but in a separate document.

Sample mortgage note for an apartment.