Recently there was news that 2-NDFL will be cancelled. But, as it turned out, officials are not yet ready for this. Find a guide to this form.

The 2-NDFL certificate form for 2021 is a document that every accountant should have on hand. First of all, it is necessary to report on the results of the year to the tax service. In addition, it is used to issue it to employees who request information about wages paid and income tax transferred.

What changed

Since the beginning of 2021, it has become known that employers and companies paying income (for example, dividends) to individuals based on the results of the current year will continue to have to report according to new rules, for which they will need a sample 2-NDFL for 2021.

The new registration procedure is significantly different from the previous one. Let's look at how to fill out, where to find and download the current Form 2-NDFL 2019. As of 01/01/2019, changes have been made that will have to be taken into account by all employers, individual entrepreneurs and organizations paying income to individuals. Based on the Order of the Federal Tax Service of Russia dated October 2, 2018 No. ММВ-7-11/ [email protected] , there will be not one form, but two. One of them is used for submitting reports to the Federal Tax Service, and the second is used for issuing to individuals who apply. As representatives of the Tax Service clarify, the sample for filling out the 2-NDFL certificate form in 2021 contains some points that are unnecessary for ordinary citizens. As for the form for the Federal Tax Service, it contains almost everything important and necessary, so the main part of the structure is preserved.

Note that both documents will have the same name - “Certificate of income and tax amounts of an individual.” But so that accountants do not get confused, a small adjustment is made:

- the report, which organizations and individual entrepreneurs must send to the tax authorities, has the abbreviation “form 2 personal income tax” in the title and the official number in the classifier of tax documents - KND 1151078;

- a document that is issued to an individual when he applies on the basis of Art. 230 of the Tax Code of the Russian Federation, has no abbreviations or numbers in the KND.

Since the purpose of the certificates is different, they have a different structure and procedure for filling out. And the Order of the Federal Tax Service directly states this. Minimal changes have been made to the form that employers must issue to employees (Appendix No. 5 of the Order of the Federal Tax Service). In particular, the line about the attribute, the adjustment number and the Federal Tax Service code and the details of the notification of the provision of a deduction were excluded from it. Since the new year, the document looks like this:

As for the report, which is submitted to the Federal Tax Service from 2021, there are slightly more changes in it. The help consists of an introductory part, two sections and one appendix. The previous form 2-NDFL had 5 sections. In addition, tax authorities removed fields for indicating the TIN of individuals and left only one field to clarify the type of notification confirming the right to one of the tax deductions.

Please note that if you fill out reports for tax authorities electronically and transfer them to the Federal Tax Service through operators, you will not notice any special changes. Intermediaries promise that they will promptly update the formats that tax agents use when transmitting data on income and personal income tax amounts. As for certificates for employees, and such requests are not uncommon, it is necessary to use new forms so as not to violate the requirements of the Tax Code of the Russian Federation.

Please note that as of 01/01/2019 the following are no longer valid:

- Order of the Federal Tax Service of the Russian Federation dated October 30, 2015 No. ММВ-7-11/485 and Order of the Federal Tax Service dated January 17, 2018 No. ММВ-7-11/ [email protected] , which now approved the working version of the document and the procedure for filling it out;

- Order of the Federal Tax Service of the Russian Federation dated September 16, 2011 No. ММВ-7-3/576 and Order of the Federal Tax Service dated December 8, 2014 No. ММВ-7-11/ [email protected] , which describe the rules on how to submit information on electronic and paper media and through telecommunications channel operators.

To submit information to the Tax Inspectorate of Moscow, St. Petersburg or another region, use our forms. To access them, registration or other additional steps are not required: all information is free for readers. It's up to you to fill out documents in word, excel or some other format.

Help 2-NDFL: what is it?

2-NDFL can be deciphered as “taxes on personal income.” It is necessary in order to certify to the tax office about the income of a particular person and the taxes that were paid on this income. This certificate is filled out and submitted to the tax office by the employer. The citizen for whom this certificate is being filled out can only receive it at work. As a rule, this does not take more than three days.

2-NDFL must have the official seal of the enterprise and its details, as well as comprehensive information about income and tax deductions for a specific employee.

What does it say

It is worth taking a closer look at what is indicated in this certificate and in what form.

- Full name of the citizen's place of work. And also all the details, codes and in general everything that relates to registration in the tax register of companies.

- Employee's passport details.

- Total income plus all deductions and tax rate.

- Not always, but other deductions may be indicated by code, in particular social or property.

- The total amount of taxes, deductions and income of an individual.

That is, from the certificate you can glean all the necessary data about the financial solvency and tax “honesty” of an individual employee.

Sample filling in 2021

Now let's look at a specific example. LLC "Company" must submit a report in 2021 for employee Semenova O.A. according to the new rules. To fill it out you must follow the instructions:

- In general information, everything is quite simple: TIN, KPP, name of the organization or individual entrepreneur, reporting year, Federal Tax Service code, reorganization code and TIN, KPP of the reorganized organization, OKTMO code, telephone.

- The certificate number is the serial number of the form sent in the reporting period.

- Sign (1, 2, 3, 4) - indicated depending on the reasons for submitting the document.

- Correction number: 00 - primary, 99 - canceling. All others from 01 to 98 are corrective reports.

- Data on taxpayers is provided from documents available to the tax agent.

- In the “Tax rate” section, you must indicate the percentage at which personal income tax is withheld. Today there are three rates: 13, 30 and 35%. The most common rate is 13%. It is used for employees with Russian resident status.

- Information on the amounts of income and calculated and withheld tax is taken for the entire reporting period.

- Deduction codes are entered taking into account the Order of the Federal Tax Service of Russia dated September 10, 2015 No. ММВ-7-11/ [email protected] In our case, code 126, since the employee has a child.

- Notification type code (provided that a notification is issued):

- number 1 is entered if the taxpayer has been issued a notice of the right to a property deduction;

- number 2, if the taxpayer has been issued a notice of the right to a social deduction;

- number 3, if the tax agent has been issued a notice confirming the right to reduce income tax on fixed advance payments.

- The application is completed for the months in which income was paid or a deduction was provided. There are no differences from the current procedure for filling out this document.

Sample of filling out the 2-NDFL certificate according to the new rules of 2019

Details about the 2-NDFL certificate

The 2-NDFL certificate is required for both employers and employees of the company. The former cannot do without it when paying taxes for an employee. The latter, without it, will not receive a loan, sick pay, social benefits and much more. What is important to know about the 2-NDFL certificate besides its main purpose?

Changes in 2021

In the new year, the 2-NDFL certificate has undergone quite serious changes. It is necessary to understand in more detail what has changed in its filling and appearance.

A serious gap in the Tax Code of the Russian Federation has been eliminated. In the 2-NDFL certificate, a special column has appeared for submitting personal income tax reports in the event of reorganization or liquidation of the company. Now the successor of the previous organization is required to handle reporting for the reorganized structure. Two new fields are used for this:

- Form of reorganization (liquidation) (code). There are seven different codes in total, from 0 to 6 (respectively: liquidation, transformation, merger, division, accession, division with simultaneous accession).

- TIN/KPP of the reorganized organization.

If the corresponding case does not happen, these fields are left empty, and the certificate is filled out as usual, but with some changes. What has changed?

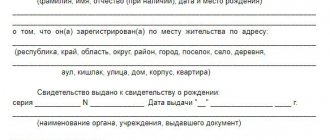

An important change in the 2-NDFL certificate: it got rid of the exact address data of the income recipient (individual). Now you do not need to fill in the employee’s place of residence. All that remains are the fields with TIN, full name, passport data and taxpayer status. In addition, the certificate no longer talks about investment deductions.

The opportunity to bring a 2-NDFL certificate on a physical digital medium (flash drive, disk, and even more so a floppy disk) was also removed. Now it can only be provided on paper or electronically (via TKS).

Common errors in the 2-NDFL certificate

Unfortunately, even in such an important document as this certificate, mistakes are often made. This can cause problems both for the individual and for the company in which he works. Therefore, it is important to carefully fill out the 2-NDFL certificate.

What are the common mistakes:

- Errors and blots on the form. You cannot correct the information included in the certificate. If an error occurs, the damaged sheet must be thrown away. The certificate is filled out on a blank form without making mistakes.

- Errors in numbers. They are associated with the inattention of the accountant who filled out the certificate and may not be detected immediately. The result may be negative consequences for the individual for whom the certificate was filled out.

- There is no signature of an authorized accountant and/or transcript in the “Tax Agent” field. The signature is made only with a blue pen. When placing a seal, it is important not to overlap it.

- The date is specified in a format other than DD.MM.YYYY. For example, MM.DD.YY.

- The stamp is placed in the wrong place. It is necessary to place it in the place where it is marked “Place for printing” (MP)

You must read this document very carefully. If received by an individual, it is recommended to check the certificate and immediately return it to the accountant if an error is noticed.

The difference between 2-NDFL and 3-NDFL

3-NDFL is not even a certificate, but a full-fledged tax return. The citizen must fill it out and submit it to the tax office independently. No one should do this for him. This declaration takes into account a person's outside income that is not related to his wages and other money received from his main employment. For example, its effect applies to the sale of an apartment if an individual has owned it for less than three years.

3-NDFL is filled out and submitted when an individual has additional income. Along with this declaration, you must also provide a 2-NDFL certificate from your main place of work.

For individual entrepreneurs, the 2-NDFL certificate is not suitable. But provided that he is not at the same time an employee. A 3-NDFL declaration has been created for an individual entrepreneur. However, it can be replaced with a certified tax return for the previous reporting period.

How long is the certificate valid?

According to Article 23 of the Tax Code of the Russian Federation, the 2-NDFL certificate is in no way limited in validity. But this does not prevent various organizations from independently establishing the scope of its “expiration date” when submitting a document, if the enterprise has established a validity period in its internal document flow.

Most often, the validity period of the 2-NDFL certificate is strictly limited. For example, banks and other credit organizations require you to bring a “fresh” document, no more than 10-30 days old.

In order for an individual to confirm his solvency, his certificate must be: current. That is, it should contain data for the last six months, ending with the closest dates to the day the document was submitted. In this case, the certificate must be drawn up correctly - the company accepting the certificate should not have any questions about its authenticity and reliability.

How do they report on past years now?

Certificates of income for individuals often undergo changes. In 2015-2016, the old form was used, approved by the Order of the Federal Tax Service dated October 30, 2015 No. ММВ-7-11 / [email protected] But at the end of 2021, the Federal Tax Service initiated consideration of the next changes to this Order in connection with the approval of the Order of the Federal Tax Service of Russia dated 17.01 .2018 No. ММВ-7-11/ [email protected] (registered with the Ministry of Justice and published on January 30, 2018). If you need to submit information for previous periods, the tax office requires you to use the forms that were in force during that period.

Form valid in 2021

Form valid in 2021

How to fill out and submit the 2-NDFL register in 2021

If the 2-NDL is submitted in paper form, it is also necessary to draw up an accompanying register in two copies . When submitting 2-NDFL electronically, you do not need to submit the register. The register is compiled according to the form found in Appendix 1 to the Procedure for filling out certificates. This Procedure was approved by Order of the Federal Tax Service No. ММВ-7-11/ [email protected] dated 10/02/2021. If the 2-NDFL certificates indicate different characteristics, then a separate register will need to be compiled for each characteristic.

The register contains the following information:

- reference number;

- name of organization, individual entrepreneur;

- attribute number;

- number of certificates;

- surnames, first names, patronymics, date of birth of individuals who appear in the certificates;

Who is required to submit certificates?

A free sample of the new 2-NDFL certificate for 2021 is required for all tax agents who are required to report to the Federal Tax Service.

They are organizations, individual entrepreneurs, other persons, in accordance with Article 226 of the Tax Code of the Russian Federation, who pay income to an individual who is a taxpayer, employees who are in labor relations with the organization, working under a contract, and other citizens. Such a person is obliged to calculate, withhold tax from the taxpayer and transfer it to the budget. The form for submission to the Federal Tax Service is filled out for each individual.

Each tax agent is obliged to ensure accounting of income paid to individuals, deductions provided to them, and taxes calculated and withheld. For this purpose, a tax register is compiled. It opens immediately upon hiring an employee. The register is developed and approved independently by the tax agent and contains information:

- about an individual, his identification data (full name, date of birth, passport details, TIN);

- types and amounts of income;

- provided deductions;

- amounts of calculated, withheld and transferred taxes;

- dates of tax withholding and its transfer to the budget, details of payment documents.

It is the data from this tax register that will be used to fill out the forms. Please note that if the organization paid the employee only benefits that are not subject to personal income tax (for example, for caring for a child under 1.5 years old), then the certificate does not need to be submitted to the Federal Tax Service.

Why do you need a 2-NDFL certificate?

For the employer, this certificate is an opportunity to provide tax information about their own employee and his tax deductions. But why might such a piece of paper be useful to an individual? After all, his superiors count everything for him and send him away.

But in fact, 2-NDFL is often required by ordinary people. The thing is that this certificate can not only help calculate taxes, but also confirm the employee’s income level. Therefore, banks often require it when applying for a loan. They want to know exactly whether the borrower is able to repay the loan taken, and whether it will then hang as a dead weight due to the client’s insolvency.

But these are not all the ways to use the 2-NDFL certificate. It may also be required in the following situations:

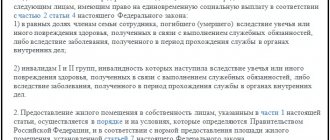

- Registration and receipt of tax deductions from the state. For example, if parents need to receive a deduction for a student who is studying on a commercial basis at a university.

- In court, if a citizen is involved in any proceedings. For example, to calculate the amount of alimony or in litigation regarding violations of the Labor Code of the Russian Federation.

- Calculation of potential old-age pension.

- Confirmation of financial status when registering adoption or guardianship.

- Filling out the 3-NDFL tax return (it is filled out based on some data from the 2-NDFL certificate).

- Obtaining a foreign visa if material support for a future trip is required.

- Calculation of unemployment benefits if a citizen is registered with employment centers.

- Receiving benefits for pregnancy and parental leave. Benefits are calculated based on the average income of the citizen over the last two years, or less if she has not been with the company for that long.

- Payment of sick leave. The cost of sick leave is also calculated using this certificate.

- Providing a 2-NDFL certificate from the old place of work to the new employer. If necessary, it is from this document that the accountant at the new place of work will calculate potential benefits and payments, since sufficient time may not have passed at the new place. In addition, standard deductions can also be calculated using the data from this document.

If necessary, an employee can contact the accounting department at any time and ask for a certificate. Moreover, it is advisable to do this in writing.

When 2-NDFL is not required

Providing a 2-NDFL certificate to the tax office is the employer’s obligation to the state. But he is not always obliged to do this. There are situations when the employee himself, and not his superiors, should be responsible for confirming income and taxes:

- When paying income on which you do not need to pay taxes. For example, social benefits or money received for the development of oppressed sectors of society.

- When paying remuneration, the individual must remit the tax on his own.

- When paying income to such taxpayers, who must independently transfer personal income tax to the tax office, without straining the employer.

In this case, the employer does not have to worry about drawing up the document. This will be done by the employee himself.

Delivery formats

When the company consists of several people, then 2-NFDL can be submitted to the tax office on paper.

If the number of individuals who received income in the company exceeded 25 people, then the report will have to be submitted only in electronic form (clause 2 of Article 230 of the Tax Code of the Russian Federation) via telecommunication channels. To prepare reports, the free software of the Federal Tax Service “Taxpayer Legal Entity” is used. To send an electronic report to the Federal Tax Service in electronic form, you must enter into an agreement with an authorized telecom operator, obtain an electronic digital signature and install software.

How to check a certificate before submitting it to the tax office electronically? To do this, just download the free Tester program from the official website of the Federal Tax Service. By installing it on your computer, you can check the file sent to the Federal Tax Service for compliance with the format for submitting the report in electronic form.

Information for Individuals

Form 2-NDFL is submitted only to the Federal Tax Service inspection at the location of the tax agent who paid the money to the individual (in the form of salary, dividends or other remuneration). For those who want to obtain information about their own earnings or find out the completeness of payment of personal income tax, the form given in Appendix 5 of the Order is suitable.

It is this paper that is necessary to receive a tax deduction, unemployment benefits, or when preparing and submitting a 3-NDFL declaration. You can obtain the document from the source of payments (employer or dividend payer). Moreover, in a short time - no later than 3 working days after the application, Art. 62 TK.

Certificate expiration date

The only deadline that is established in tax legislation in relation to form 2-NDFL is the deadline for submitting a report to the Federal Tax Service - before March 1. The Tax Code of the Russian Federation says nothing about its shelf life.

In general, the validity period of the document is usually 30 calendar days. However, in the case of documents on the amount of annual cash receipts, this period may vary:

- to assign an allowance based on average earnings or provide benefits - until the end of the month in which the paper was issued;

- for sick leave - valid without limitation, but will be relevant only until the person has worked for the current employer for 2 full calendar years (from January 1 to December 31);

- when submitted to commercial organizations or visa departments of foreign embassies, the deadlines are set in each case separately.

Report submission deadlines

Please note that you must fill out and submit 2-NDFL to the tax office no later than April 1 of the year following the reporting year.

Since this is the last date when tax agents transmit information about an individual’s income, calculated, withheld and transferred taxes to the budget (clause 2 of Article 230 of the Tax Code of the Russian Federation). In this case, the number 1 is indicated in the “Sign” field. In 2021, April 1 fell on a Sunday, so the deadline was postponed to 04/02/2018. As for 2021, no transfers are provided. If the tax agent was unable to withhold tax when paying income and during the entire tax period, then he is obliged to provide the tax report, indicating the number 2 in the “Sign” field. This must be done before March 1 of the next year (clause 5 of Article 226 of the Tax Code RF). Please note that the procedure for providing such information to the tax authorities is now presented in Appendix No. 4 to Order of the Federal Tax Service of Russia dated October 2, 2018 No. ММВ-7-11/ [email protected]

For late submission of the report, a liability of 200 rubles is provided. for each certificate (clause 1 of Article 126 of the Tax Code of the Russian Federation), that is, for a form drawn up for an individual employee. Responsibility has also been introduced for providing certificates with false information. For each such report you will have to pay a fine of 500 rubles. (Article 126.1 of the Tax Code of the Russian Federation), and it can be avoided only if the tax agent identifies and corrects the error before it is discovered by the tax authority.

Information for legal entities and individual entrepreneurs

Employers from among organizations or individual entrepreneurs must annually submit to the Federal Tax Service at their location data on the amounts of accrued wages and withheld tax with a breakdown for each recipient and month of payment (2-NDFL). This must be done no later than March 1 of the year following the billing year. This form is submitted exclusively to the tax office and is not given to employees. A message about the amount of income tax transferred by the agent or about the impossibility of withholding is sent to the recipient of the income using the form from Appendix 5.

Certificate to the Federal Tax Service: submission

Tax agent reporting is submitted electronically or in paper form. The last option is available only to those who, during the year, have entered into employment or civil law relations with no more than 10 individuals.

When submitting 2-NDFL on paper, the reporting package is supplemented with a register of all provided copies. The person responsible for receiving reports must conduct preliminary control and check:

- availability of fixes;

- complete completion of all basic details, indicators of income and deductions;

- presence of the company seal and signatures of the persons responsible for filling it out.

Those who received more than 10 certificates at the end of the year must submit information using telecommunication channels and a qualified digital signature.

Certificates 2 personal income tax under GPC agreements with individuals

Reporting on paid earnings and withheld personal income tax is submitted not only for persons with whom an employment contract has been signed. If a business entity has civil legal relations with individuals, then information about them must also be submitted to the Federal Tax Service.

In this case, there can be two options:

- the reporting indicates the amount of income withheld for each of the agreements;

- A message about non-withholding of personal income tax is sent to the tax office and the recipient of the funds.

In the latter case, the contractor is obliged to take care of declaring and paying fiscal obligations to the budget.

Due dates

The local division of the Federal Tax Service and the recipient of funds must be informed about the amount of accrued annual income and income tax transferred to the budget before March 1 of the year following the reporting year, Articles 226 and 230 of the Tax Code.

Fines

Late submission of the annual 2-NDFL or errors in its preparation will be punished financially:

- according to Art. 126 Tax Code - 200 rubles for each unsubmitted certificate;

- according to Article 15.6 of the Administrative Code - up to 500 rubles for officials or individual entrepreneurs;

- according to Art. 126.1 Tax Code - 500 rubles for each document containing an error, if the tax agent himself did not have time to correct it.

When not to submit

There is no need to submit data to the Federal Tax Service if payments:

- were made to the individual entrepreneur;

- are not included in the list of income subject to personal income tax;

- are dividends for shareholders (participants of a public or non-public JSC);

- made as part of the execution of an assignment or commission agreement;

- are in the nature of material assistance or a gift, costing no more than 4,000 rubles per year.

Income and deduction codes

The most common code for income received in the 2-NDFL certificate is 2000 (remuneration for the performance of labor duties). However, each type of accrual and deduction has its own code value. A complete list of types of income and deductions, as well as a table of codes with an explanation of their meanings, is given in the Order of the Federal Tax Service No. ММВ-7-11 / [email protected]

Revenue codes

Deduction codes

Zero certificate

Zero indicators in the 2-NDFL form may appear in two cases:

- paid income is not subject to income tax - data is not submitted to the Federal Tax Service;

- the fiscal agent failed to withhold personal income tax upon payment (for example, if it was made in kind) - reporting is submitted before March 1.

What changes has the uniform undergone in 2021?

The changes are mainly technical and do not affect the procedure for reflecting income, deductions and taxes:

- Section 1 contains information about the reorganization or liquidation of the company;

- Section 2 excludes information about the taxpayer’s place of residence;

- Section 4 excludes references to investment deductions;

- in section 5, in the lines of the signature and certifying the authority of the signatory of the document, a mention is made of the possibility of signing the certificate by the legal successor.

Thus, filling out the main sections remains the same.

Sample of filling out a certificate in 2021

Before downloading the 2-NDFL certificate form to fill out in 2021, we recommend that you familiarize yourself with the rules in force in 2021 (until December 31):

- In section 1, you must indicate the name of the tax agent and his basic details: TIN, KPP, OKTMO code.

- Section 2 contains information about the individual: his full name, date of birth and passport details. As mentioned above, you do not need to indicate your residence address.

- Section 3 reflects the taxpayer’s income, graduated by month of payment, income code, and amount.

- Section 4 should provide information about tax deductions provided to individuals.

- The total amounts for the year: income and deductions of an individual, taxes calculated, withheld and transferred to the budget of the Russian Federation are reflected in section 5. The details of the person responsible for filling out are also indicated here.

- Section 3 is completed for each tax rate. For example, if an employee is a non-resident and receives dividends, then two sections 3 and two sections 5 of the certificate must be completed for him. Separately - for wages at a rate of 30% and separately - for dividends at a rate of 15%, indicating the income code.

Sample certificate 2-NDFL according to the 2021 form

Dividends in the certificate in 2021

If the company paid dividends to individual founders in 2021, then certificates must also be drawn up for them and submitted to the Federal Tax Service. The dividend income code in the 2021 report is 1010. The tax rate can be:

- 13% if the participant is a resident;

- 15% if the participant is a non-resident of the Russian Federation.

If the founder of the company who received the dividends is a resident of the Russian Federation and at the same time receives wages in the company, then the dividends should be reflected in the same section 3 as other income. In this case, there is no need to fill out a separate section 3.